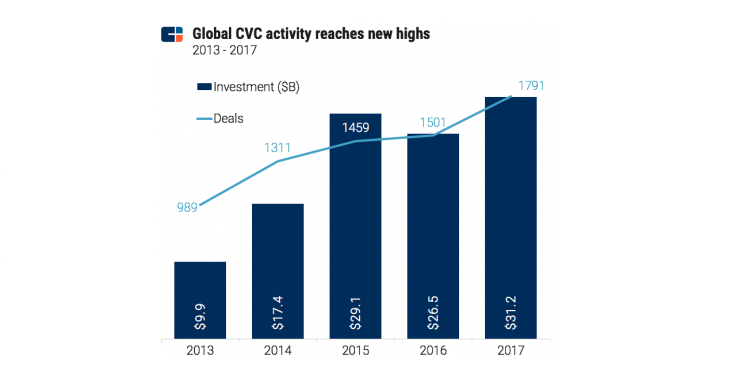

2017 saw another year in the increase of corporate investing in startups across the globe.

$31.2B was invested across 1791 deals in 2017. The secular trend is an increasing appetite for risk among corporates as they make bets across a number of strategic areas, whether it is e-commerce for retail, autonomous navigation for car manufacturers, fintech for the traditional financial services companies or artificial intelligence and machine learning for the overall tech sector.

The two by two matrix: “strategic fit” or “financial returns” on the y-axis and “eyes and ears” or “leveraged R&D” on the x-axis still holds good for most CVCs. A few CVCs such as Sapphire ventures (formerly SAP ventures) have changed their model to focus entirely on financial returns and have even diversified their LP base from the corporate balance sheet to external LPs.

However, key differences still remain compared to institutional venture capital, where financial returns is the one and only goal and compensation is highly aligned with that goal. CVCs have had a tough time attracting the top talent because of the compensation challenges they face compared to traditional VCs.

Nevertheless, the decision to choose to take money from either CVCs or institutional VCs has some nuances for an entrepreneur. There are four considerations:

1.Talent:

As much as CVCs tout their ability to company building, they would rather hire the top talent themselves than let their portfolio companies. Also, most CVCs just don’t have the same panoply of professionals that help their portfolio companies in recruiting top talent.

2.Top line:

CVCs can open doors to their internal business groups which can be helpful for startups to secure OEM or revenue sharing contracts. Nothing like having a channel sales deal that leverages a large existing sales force to sell products.

3.Technology:

a CVC can bring major resources from its parent company to perform technology due diligence which a normal VC cannot. A validation of such sort can be very comforting to other investors which may lead to securing capital in fund raising, especially when the startup does not have a large revenue base.

4. Timing:

CVCs are notorious in taking their sweet time to get approvals from their countless committees and checks and balances from their organizational labyrinth. Thus, unless it is the last resort, as in the case of most hardware startups, it is easier for startups to raise money faster from traditional VCs. 5. T’s & C’s: if the strategic fit with the startup is right, then the T’s and C’s are very important when it comes to ROFR (right of first refusal), ROFO (right of first offer), ROFI (right of first information), not to mention the veto rights, and dragging rights, depending on how much capital CVCs invest. Most corporates want explicit or implicit exclusivity and it is the entrepreneur’s responsibility to stay clear of all tie ups that limit their upside.